This is the tenth article in a series where I examine the structural conditions that would need to change for Europe to function as a genuinely independent strategic actor.

In the previous article I established that the pharmaceutical and medical supply chains required to treat battlefield casualties at the scale a high-intensity European conflict would generate cannot meet that demand under European sovereign production. The active pharmaceutical ingredients for the most critical medicines, the anaesthetics, the antibiotics, the blood products and their stabilizers, trace upstream to root inputs and synthesis steps that are predominantly produced in China and India, and in several categories European sovereign production is effectively zero.

The structural finding was that Europe could find itself unable to keep its wounded alive in sufficient numbers because of a shortage of the chemical compounds required to produce the pharmaceuticals and medicines to treat them, and that chemistry shortage has been invisible in every European defense planning document because the conversation has been conducted at the clinical and logistics level rather than at the industrial and supply chain level where the actual constraints sit.

In this article I trace the main chemistry supply chain for European ammunition and drone warhead production, identify where European sovereign production exists and where it does not, and assess what closing the gaps would actually require. The analysis includes drone warfare, because any assessment of what Europe would need to sustain a conflict that does not treat drones as a primary mode of combat is working from an outdated model of what high-intensity conflict now looks like.

Several of the most important supply chain gaps in European ammunition production have existed for decades, and in some cases since the industrial system that produces ammunition was first designed, and they have remained invisible in the policy conversation because the conversation has been conducted at the wrong level of the supply chain. If the question is whether Europe can produce enough shell casings, the answer is improving. If the question is whether Europe controls the chemistry that has to exist before a shell casing can be loaded, the answer is mostly no, and in several critical categories, no without qualification.

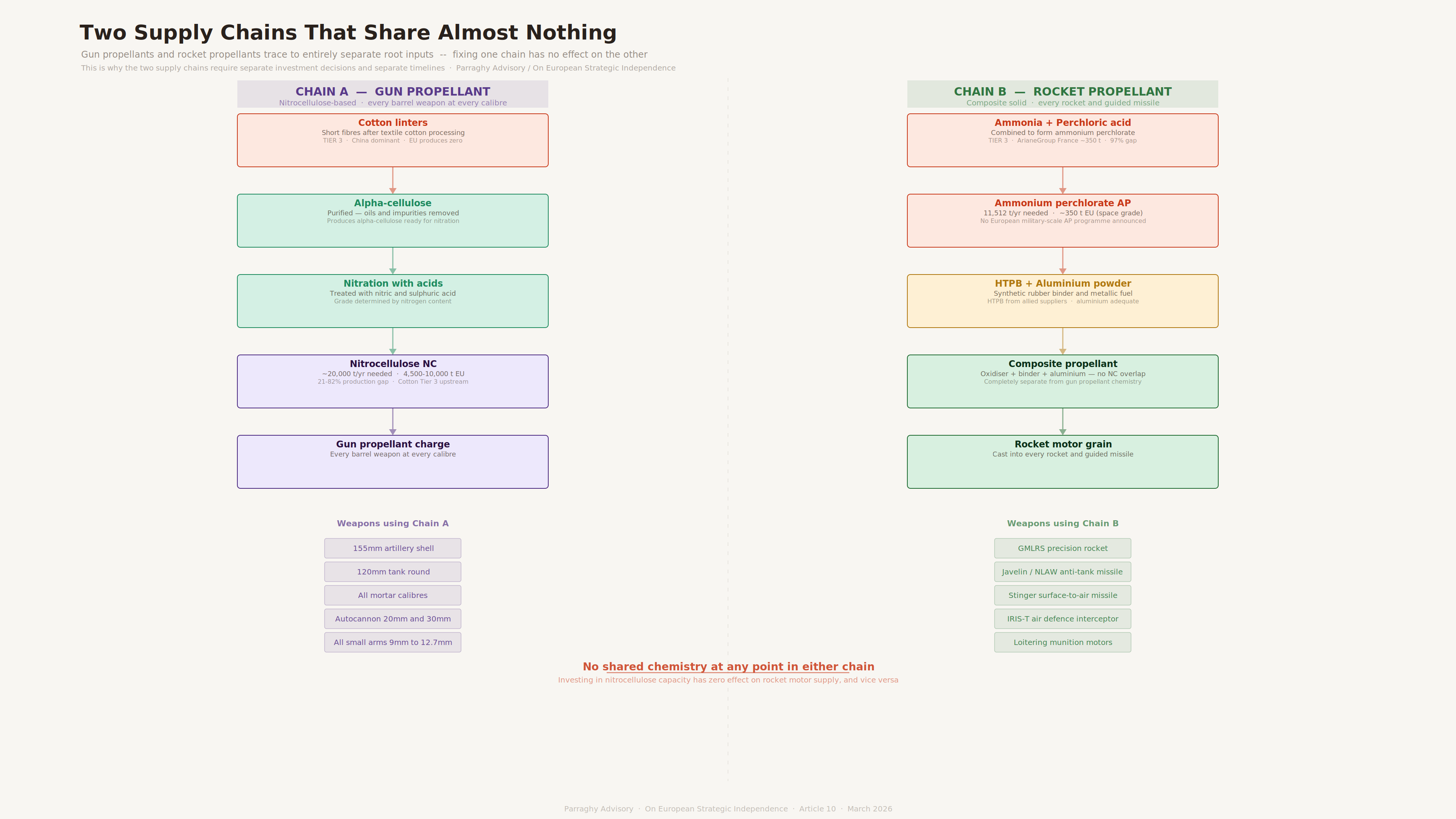

Two propellant families, two entirely separate supply chains

The first thing to understand about ammunition chemistry is that there are two supply chains, and they share almost nothing upstream of the gun or rocket motor.

Virtually every weapon that fires a projectile from a barrel uses a nitrocellulose-based propellant. Nitrocellulose is a highly reactive form of cellulose, the structural fiber found in plant cell walls, produced by treating purified cotton fiber with nitric acid and sulphuric acid under carefully controlled conditions.

The chain runs from raw cotton through a purification stage that removes oils and impurities, producing alpha-cellulose, which is then nitrated to produce nitrocellulose in one of two grades depending on nitrogen content, with the higher-nitrogen grade used for propellant applications and the lower grade used for other industrial purposes. This chemistry underpins every artillery shell, every tank round, every mortar round, every autocannon round, and every cartridge fired from a rifle, machine gun, or pistol, regardless of caliber.

Every rocket and guided missile uses a different family of propellant entirely. Composite solid propellants consist of an oxidizer, which provides the oxygen needed for combustion in the absence of atmospheric air, a binder that holds the propellant grain together and itself contributes to the energy output, and in most formulations a metallic fuel powder that increases energy density.

The oxidizer is ammonium perchlorate, a white crystalline compound produced from ammonia and perchloric acid. The binder is HTPB, hydroxyl-terminated polybutadiene, a synthetic rubber, and the metallic fuel is aluminium powder. This chemistry powers every GMLRS precision-guided rocket fired from HIMARS or MLRS platforms, every Javelin and NLAW anti-tank guided missile, every Stinger shoulder-fired surface-to-air missile, MANPADS being the military abbreviation for a man-portable air defense system meaning a missile light enough for one soldier to carry and fire, and every IRIS-T air defense interceptor. None of these weapons share any production infrastructure with gun-fired ammunition at the propellant level.

This matters for investment planning because the two supply chains must be addressed separately. Expanding nitrocellulose production capacity, which is one of the things European investment is actually doing, has no effect on the rocket motor propellant supply situation. And the rocket motor situation is substantially worse than the gun propellant situation, because ammonium perchlorate production in Europe exists primarily to serve the commercial space sector rather than military applications, at a scale that is roughly 3% of what a sustained high-intensity conflict would require.

What goes inside a round

Beyond the propellant that fires it, most rounds also contain an explosive filler in the warhead, and a detonating chain that initiates that filler on impact or command. These add further chemistry that traces to further supply chains.

The explosive filler in artillery shells and most other bursting munitions is typically a composition called Comp B, which is a mixture of RDX and TNT in roughly a 60-40 ratio by weight. RDX, whose full name is cyclotrimethylenetrinitramine and which is sometimes called hexogen, is a white crystalline primary explosive that provides most of the destructive energy, and TNT, 2,4,6-trinitrotoluene, is slightly less sensitive and acts as a desensitizer and energy contributor.

RDX is produced by reacting hexamine, itself produced from ammonia and formaldehyde, with nitric acid under controlled temperature conditions. TNT is produced by nitrating toluene, a petroleum derivative that arrives as a by-product of crude oil refining and coal tar processing.

The detonating chain is a further set of chemistry, consumed in gram quantities per round but functionally non-negotiable. The primer, which initiates the propellant charge when the firing pin strikes it, contains lead styphnate, a lead salt of styphnic acid produced from resorcinol through a multi-step nitration process. The fuze detonator, which initiates the explosive filler on impact, contains lead azide, produced by reacting lead nitrate with sodium azide. Without functioning primers and detonators, no round fires regardless of how much propellant and explosive filler is available.

They are the ignition chain that everything else depends on, and their volumes are so small that they have been invisible in every supply chain analysis conducted at the platform or production-volume level.

Drone warheads draw on the same explosive chemistry. First-Person-View (FPV) kamikaze drone warheads typically use an RDX-based or TNT-based filler. Loitering munition warheads, which are heavier and more varied, use plastic-bonded explosive formulations in which RDX crystals are suspended in a rubber or polymer binder to improve handling safety and battlefield performance, and those formulations are predominantly RDX-based and used in precision munitions. Long-range strike drones of the type Ukraine has deployed extensively, analogous to Iran's Shahed-136, carry warheads of 40 to 50 kilograms that are broadly similar in composition to large artillery shell fillers.

The drone warhead demand adds to the same chemistry pools that artillery and infantry weapons draw on, which means that a shortage in RDX production capacity affects the entire system simultaneously, not just one weapon category.

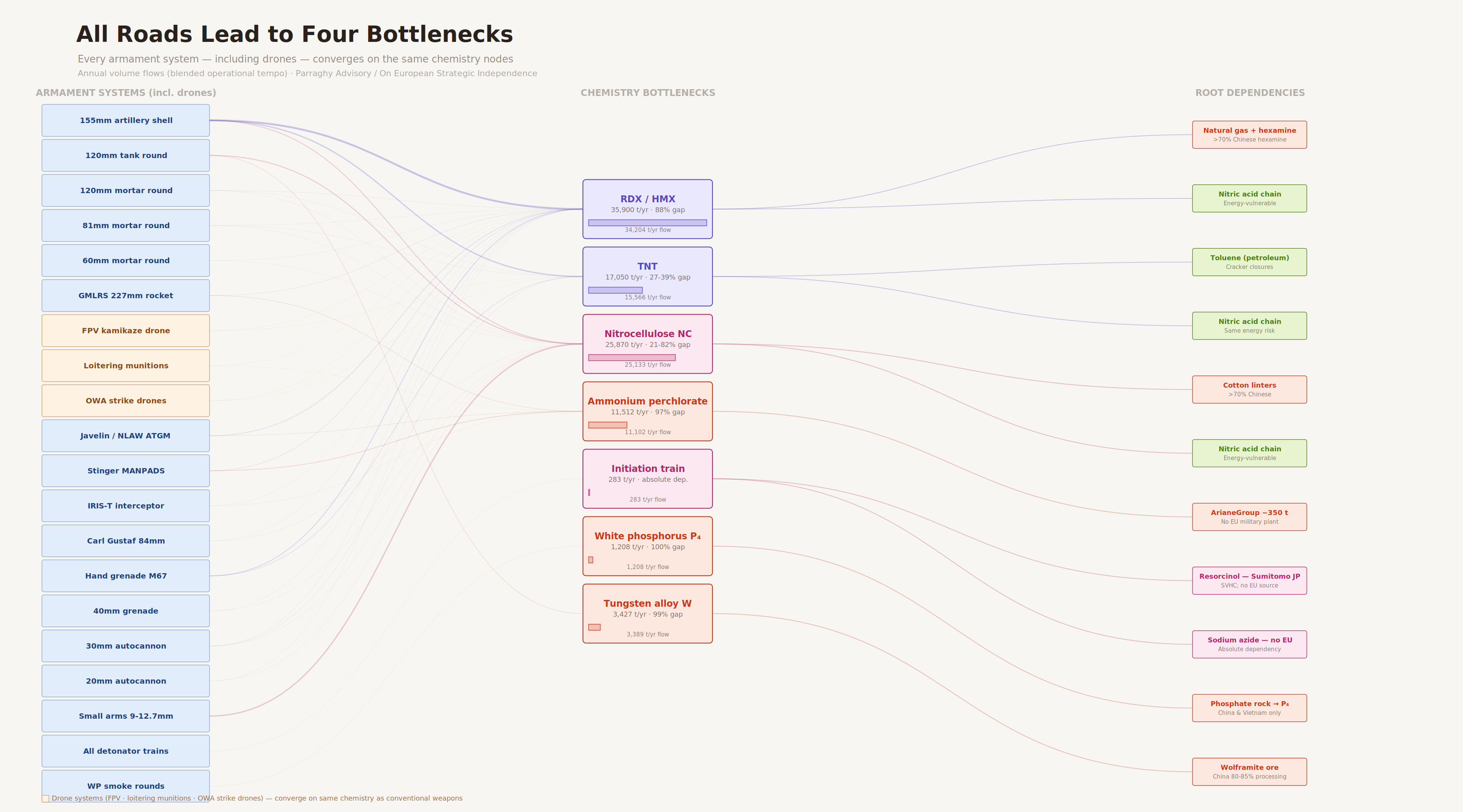

The convergence of the chemistry bottlenecks

The supply chain situation would be complicated but manageable if each weapon system depended on a unique chemistry. The actual situation is worse, because most weapons share chemistry upstream, which means a disruption at a shared node affects all of them at once.

The convergence diagram above shows this structure directly. Artillery shells, hand grenades, tank rounds, FPV drones, Javelin missiles, loitering munitions, and mortar rounds all flow upstream through RDX. Nitrocellulose serves every gun-fired category without exception. Ammonium perchlorate serves every rocket and missile simultaneously. When a supply chain node is disrupted, the disruption propagates across every weapon category that depends on it, and there is no substitution possible within the compressed timeframe of an active conflict.

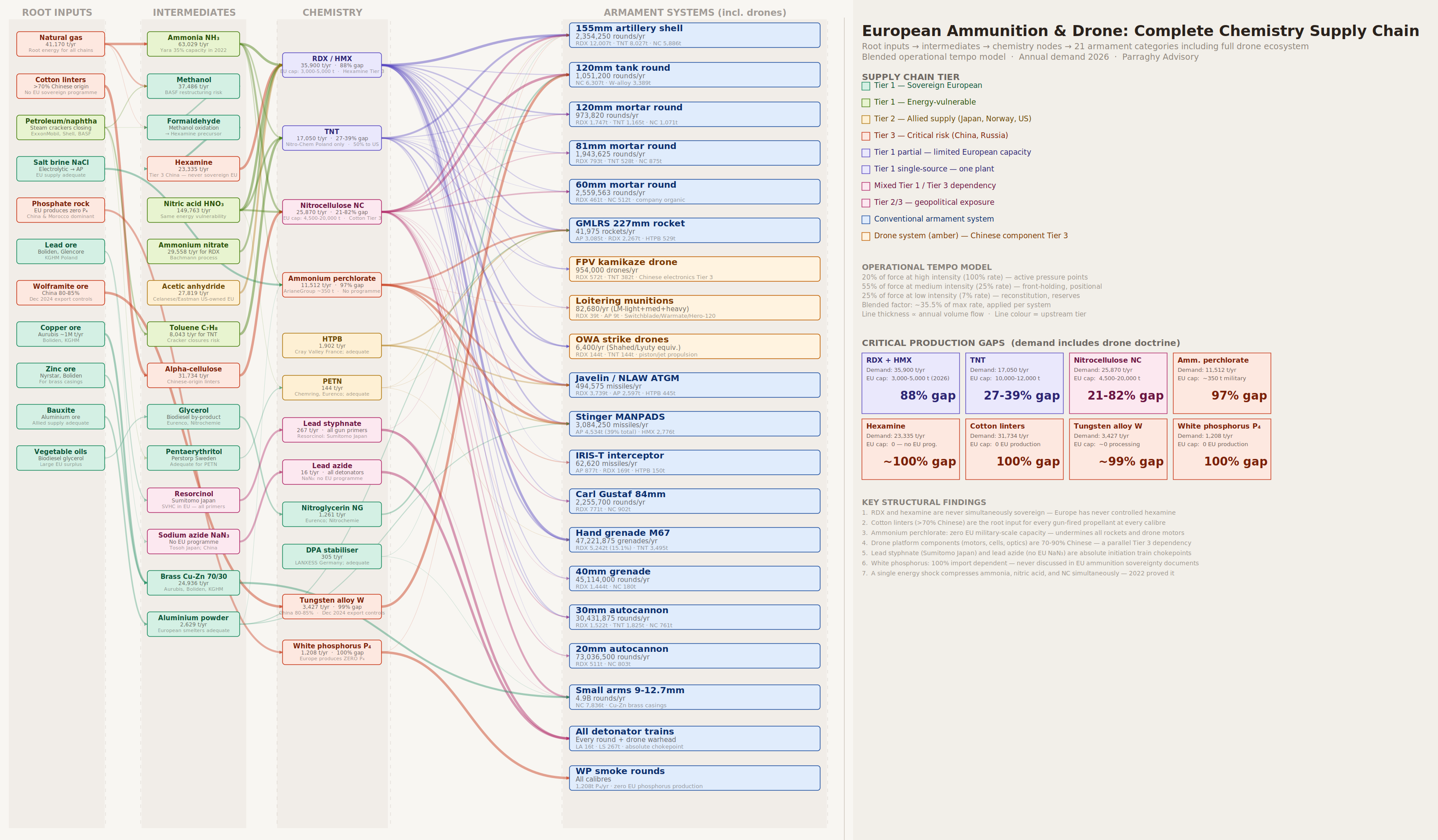

The full supply chain, from root industrial inputs through intermediate chemistry to finished armament systems, can be traced in the diagram below.

Reading this map at the supply chain level rather than the platform level surfaces four findings that do not appear in any publicly available European ammunition sovereignty analysis reviewed for this research.

Cotton is a defense-critical industrial material, and Europe produces none of the specific grade required. Every gun-fired propellant chain begins with cotton linters, the short fibers left after the long fibers have been separated for textile use. Those linters are purified into alpha-cellulose and then nitrated to produce nitrocellulose. China is the dominant source of cotton linters and accounts with over 70% for the majority of what is traded globally, with the United States, India, and Pakistan as secondary producers. Europe produces none.

Europe has no domestic production and no announced program to develop one. Alternative feedstocks based on wood pulp exist and are technically viable, but the industrial transition to wood pulp cellulose for propellant-grade nitrocellulose has not been initiated at European scale. Expanding shell assembly capacity without addressing the cotton linter dependency is expanding the downstream end of a supply chain whose root is structurally compromised.

Hexamine is an organic crystalline compound produced from ammonia and formaldehyde, and it is the key feedstock in the production of RDX. Europe does produce hexamine commercially, for applications such as resins, fuel tablets, and pharmaceuticals, but that civilian production has never been scaled or secured for the volumes that military-grade RDX production at conflict scale would require. The dependency for the specific military application has simply migrated between unreliable geographies.

Before 2022, significant supply of the hexamine used in European RDX production came from Russian producers, warehoused and distributed through intermediaries in Poland and elsewhere. After 2022, that supply shifted primarily to Chinese producers. While the geographic origin changed, the structural character of the dependency did not. Europe has never had sufficient sovereign hexamine capacity for military-scale RDX production, and building that capacity has not become a policy priority.

Ammonium perchlorate production in Europe is calibrated for the space industry rather than for military applications. The only European facility producing military-grade ammonium perchlorate at any scale is operated by ArianeGroup in France, producing approximately 350 tonnes per year. Against a conflict-scenario demand of 11,512 tonnes per year for current-inventory force structure alone, that represents roughly 3% coverage. No new European military-scale ammonium perchlorate production program has been announced.

The drone platform supply chain introduces a parallel Tier 3 dependency, which is supply that originates from countries whose reliability under conflict, geopolitical pressure or when their and European interests are not aligned, cannot be assumed, that is structurally identical to the cotton linter problem but operates through an entirely different industrial chain. FPV kamikaze drones and quadcopter-type systems depend on brushless electric motors, lithium-polymer battery cells, camera modules, video transmitters, and flight controllers.

Approximately 80% of brushless motors and electronic speed controllers come from Chinese manufacturers. Approximately 75 to 85% of lithium-polymer battery cells are Chinese-produced. Around 90% of the FPV-specific camera modules used in drone racing and combat FPV applications come from Chinese producers such as Runcam and Caddx. Flight controller hardware is 65 to 70% Chinese.

These components have no military supply chains in the traditional sense, because FPV drones developed as a consumer product before becoming a weapon. Europe does not produce them at scale in any tier classification, and no sovereign European production program has been publicly announced for any of these components. A European force that has addressed the explosive chemistry gaps but not the drone platform components can produce warheads it cannot deliver, and a force that has drone manufacturing capacity but not the chemistry cannot arm them. The two problems require simultaneous resolution, not sequential.

What Europe currently has and what the gaps look like

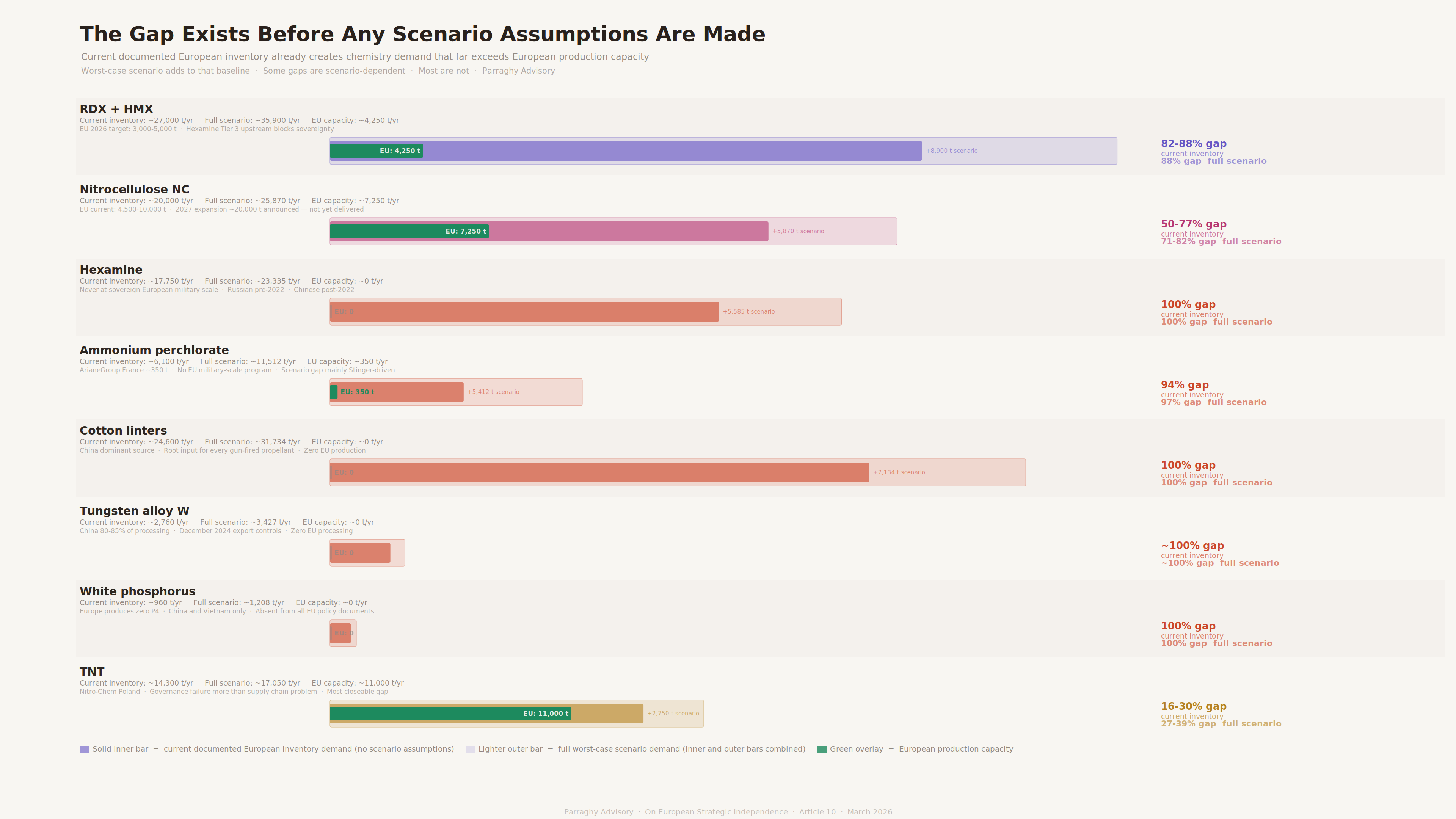

The production gap analysis presented below is based on two separate assessments that should not be conflated. The first is what chemistry demand arises from the platforms European NATO members currently hold in their documented inventory. This requires no scenario assumptions and no mobilization projections. It is simply the chemistry required to sustain what already exists. The second is the demand that arises under a full worst-case conflict scenario with one million deployed ground forces, which incorporates systems that would require years of procurement before the chemistry constraint even becomes binding.

The documented serviceable European NATO artillery inventory is approximately 800 to 1,200 155mm howitzers depending on the assessment of readiness rates. Modern capable main battle tanks, meaning Leopard 2 variants at A5 or above, Leclerc, and Challenger 2, number approximately 1,200 to 2,000 across all European NATO members. GMLRS-capable launch systems, including German MARS II, British M270, French LRU, Italian HIMARS, and the Baltic states' newly delivered systems, total approximately 180 to 250 launchers, of which this research assesses roughly 60 as likely deployable given the state of operational rocket stocks after substantial transfers to Ukraine. The Stinger MANPADS situation is the starkest of all, with Germany having donated approximately 2,700 missiles, the United Kingdom approximately 2,000, the Netherlands several hundred, and other European nations additional quantities.

Based on publicly confirmed donation figures and estimated pre-donation stockpile levels, the remaining European Stinger inventory across all nations is assessed at below 15,000 missiles, which at any sustained conflict firing rate represents days of consumption rather than months. This is a research estimate rather than an officially published figure, and the actual number may be lower given that some national donation totals have not been publicly confirmed.

Against that current documented inventory, without any additional procurement and without any force expansion, the chemistry demand is already far beyond European sovereign production capacity for most critical nodes. RDX demand from current inventory alone is in the range of 27,000 tonnes per year, derived from the consumption calculations for each weapon system in the documented inventory. European production capacity in 2026 is targeted at 3,000 to 5,000 tonnes per year, which is an 82 to 88% gap. Nitrocellulose demand from current inventory is roughly 20,000 tonnes per year against current European capacity of 4,500 to 10,000 tonnes, a gap of 50 to 77% that the announced 2027 expansion to 20,000 tonnes would theoretically close if the targets are met on schedule. Ammonium perchlorate demand from current inventory is approximately 6,094 tonnes per year against 350 tonnes of European military-grade capacity, a 94% gap. Cotton linters and hexamine are 100% gaps at any inventory level because European production is zero.

The worst-case scenario with full mobilization, the drone ecosystem fully built out, and Stinger and IRIS-T at the assumed scale adds further chemistry demand on top of those current-inventory figures. The scenario-level RDX demand rises to 35,900 tonnes per year, reflecting the addition of drone warheads and the expansion of infantry and artillery forces. The NC demand rises to 25,870 tonnes. Ammonium perchlorate rises to 11,512 tonnes, with the increase driven almost entirely by the assumption of 5,000 Stinger teams firing at sustained rates, which is a procurement-dependent figure rather than a current reality.

The point is not that the scenario figures are wrong as a planning horizon. The point is that the current-inventory figures already reveal a crisis that requires no scenario assumptions at all.

Three findings that are not in the policy conversation

Three specific findings from the supply chain analysis are worth stating separately because they are structurally important and absent from every European ammunition sovereignty document reviewed for this research.

The first concerns hand grenades. The M67-type fragmentation grenade and its European equivalents use Comp B filler, the same RDX-TNT mixture as artillery shells. Under the blended operational tempo model, which distributes consumption across high-intensity, medium-intensity, and low-intensity phases of a sustained conflict rather than assuming continuous maximum firing rates, the annual hand grenade demand generates approximately 5,242 tonnes of RDX consumption. That figure exceeds the combined RDX demand from all Javelin and NLAW anti-tank guided missiles fired across the same period.

The hand grenade is the second-largest single RDX consumer in the entire weapons inventory after 155mm artillery shells, yet it does not appear in any European RDX supply chain analysis because the policy conversation has focused on precision and long-range weapons rather than on the high-volume infantry weapons that collectively dominate chemistry demand by mass.

The second concerns TNT. The TNT production gap, at 16 to 30% against current inventory demand and 27 to 39% at full scenario scale, is structurally different from every other gap in the analysis, because it is in principle closeable within a much shorter timeframe and at a much lower cost than the other critical nodes.

Nitro-Chem in Poland has meaningful production capacity. A second European TNT production facility, which does not require the same permitting complexity or construction lead time as an RDX or ammonium perchlorate plant, would close the gap. The reason this has not happened is that Nitro-Chem's existing output is substantially committed to the US market through existing contracts, and no European industrial policy decision has been made to redirect or expand that capacity for European sovereign use. The TNT gap is a governance problem wearing the clothes of a supply chain problem, and it is therefore the most immediately actionable finding in this analysis.

The third concerns what I will call the ignition chain. Every round that fires, at every caliber, requires a primer that initiates the propellant and a detonator that initiates the explosive filler. The primer contains lead styphnate as its primary explosive compound. Lead styphnate is produced from resorcinol through a multi-step nitration process, and the principal global industrial supplier of resorcinol at the purity and volume required for lead styphnate production is Sumitomo Chemical in Japan. The detonator contains lead azide, produced by reacting lead nitrate with sodium azide, and there is no sovereign European production program for sodium azide at military scale. Chemring in the United Kingdom produces some lead azide, but the upstream dependency on sodium azide from Japanese and Chinese suppliers remains.

The annual demand for lead styphnate across all gun-fired rounds at conflict tempo is approximately 267 tonnes. The annual demand for lead azide is approximately 16 tonnes. These are small numbers, which is precisely why they have been invisible in a policy conversation calibrated to think about supply chain problems in terms of volume, but the strategic significance of these compounds is categorical rather than proportional.

If resorcinol supply from Sumitomo is disrupted, no primer can be produced in Europe, and no gun fires regardless of how much RDX, TNT, or nitrocellulose is available. If sodium azide supply fails, no lead azide can be produced, and no fuze detonator can be loaded. The ignition chain is an absolute chokepoint that sits at gram-scale volumes and therefore at the very bottom of every supply chain priority list, which is precisely where it should not be.

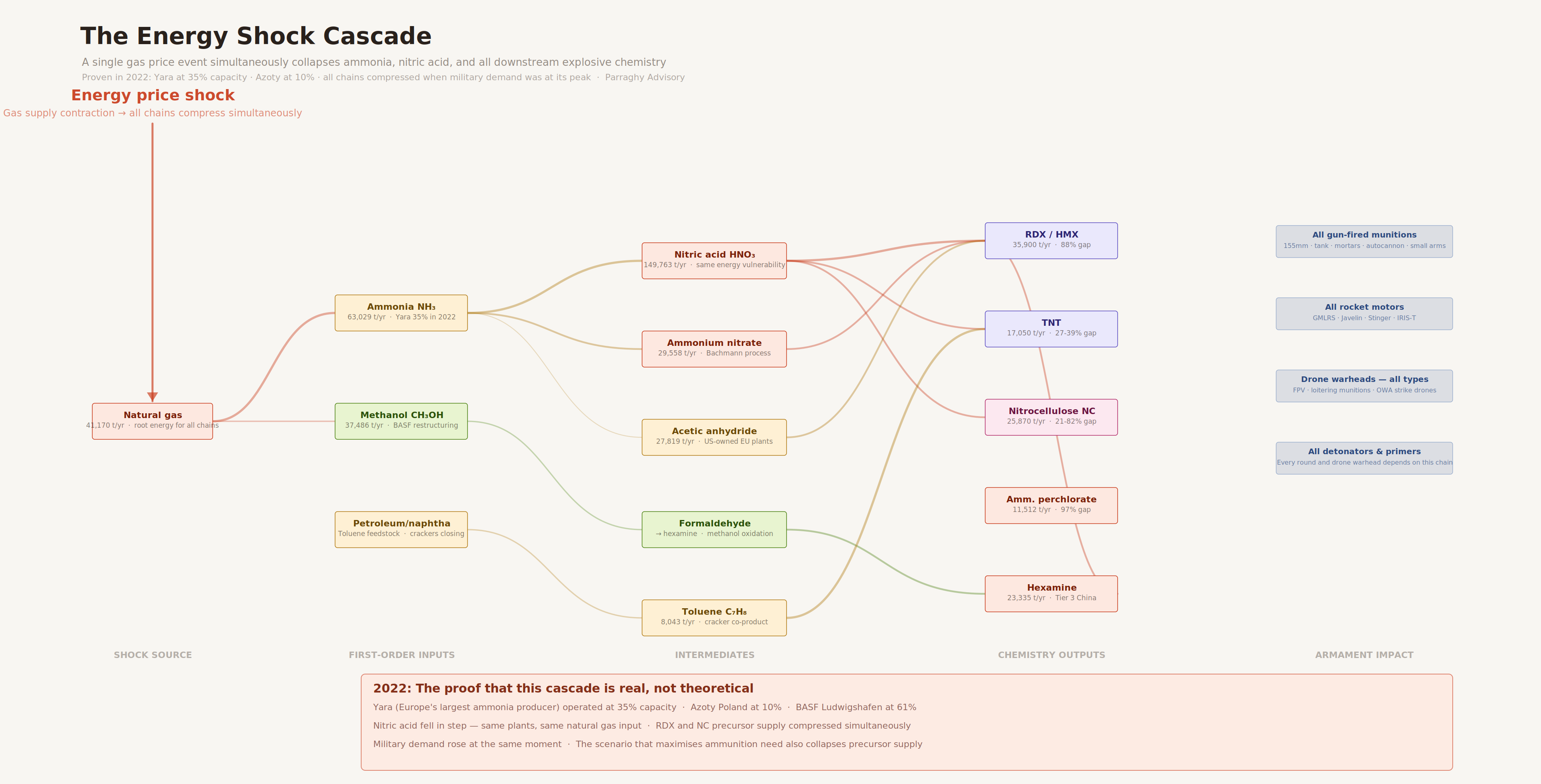

The energy problem

The supply chain vulnerabilities described above are structural in origin. There is a separate but related vulnerability that is dynamic, meaning it activates under the conditions that already maximize pressure on the system.

In the second half of 2022, European natural gas prices rose sharply as Russian pipeline supply was curtailed. Yara, a Norwegian company and Europe's largest producer of ammonia and among the largest producers of nitric acid, responded by reducing output to approximately 35% of capacity. Azoty, Poland's major nitrogen chemistry group, ran at approximately 10% of capacity. BASF at Ludwigshafen reduced methanol and downstream chemical output substantially. Nitric acid production across Europe fell in step, because nitric acid is produced from ammonia at the same facilities through a chemical oxidation process, meaning any disruption to ammonia supply immediately reduces nitric acid output as well.

The reason this matters is not the 2022 event itself but the structural relationship it revealed. Ammonia is the upstream input for nitric acid, which is in turn an upstream input for RDX, for nitrocellulose, and for TNT through its role in nitrating toluene. A disruption in natural gas supply, by compressing ammonia production, simultaneously compresses every chemistry chain that flows downstream from it. The compression affected all chains at the same time, because they all draw on the same upstream input at the same moment.

The strategic significance of this is that the scenario which maximizes European military demand for ammunition chemistry is also the scenario most likely to compress the upstream supply of that chemistry. A large-scale conflict involving Europe would generate the political and physical conditions most associated with energy supply disruption, and energy supply disruption cascades downward through the ammonia and nitric acid chains into explosive chemistry production. These two effects are positively correlated by the underlying causal structure of the system.

The 2022 event is therefore not merely a historical data point about commodity price volatility, but the proof that the cascade is real and reproducible, and it occurred during a period when military demand was already increasing rather than stable. Planning for European ammunition sovereignty without accounting for this structural correlation is planning based on a model that available evidence has already invalidated.

The drone ecosystem as a demand layer

Ukraine's experience has established empirically what drone-based warfighting actually requires and consumes, and the figures are large enough to reshape the ammunition chemistry picture materially.

By end-2024, Ukraine was producing approximately 200,000 FPV kamikaze drones per month, having scaled from near-zero production in early 2022 through a distributed manufacturing model involving approximately 500 producers of varying scale.

A March 2025 analysis by iStories, an independent Russian investigative outlet, reported on findings by Russian field medics showing that in positional, lower-intensity phases of combat, roughly three quarters of Russian soldier injuries were caused by FPV drone strikes rather than by conventional artillery. A December 2025 study by the US Army placed the broader share of all combat casualties in Ukraine that could be attributed to drone systems at between 60 and 80%.

Of the 31 Abrams tanks the United States supplied to Ukraine, Oryx, the open-source research group that tracks only equipment losses it can confirm with visual evidence, had documented at least 23 as destroyed, damaged, or abandoned by mid-2025, the majority attributable to drone strikes based on available footage. The New York Times, citing Ukrainian officials, reported 19 of the original 31 had been taken out of service. The remaining operational Abrams were withdrawn from frontline positions because their vulnerability to fiber-optic-guided FPV drones made forward deployment unsustainable.

The drone ecosystem relevant to this chemistry analysis consists of five distinct categories with different chemistry profiles.

FPV kamikaze drones carry warheads averaging approximately one kilogram of RDX-based or TNT-blend explosive, operate at consumption rates that, when scaled to a comparable force structure and distributed across the mix of high-intensity, medium-intensity, and low-intensity operational phases that characterise a sustained conflict rather than assuming maximum firing rates throughout, correspond to approximately 954,000 per year, and generate roughly 572 tonnes of RDX demand and 382 tonnes of TNT demand annually at that scale.

Loitering munitions, which are purpose-built systems that can identify and engage targets autonomously or under operator guidance, range from squad-level systems with warheads equivalent to a 40mm grenade up to heavy anti-armor systems with warheads of approximately five kilograms using PBXN-series formulations that are primarily RDX-based. At scenario scale, the loitering munition category adds approximately 39 tonnes of RDX and nine tonnes of ammonium perchlorate demand annually, the latter coming from the solid propulsion motors in medium and heavy variants.

Quadcopter-type platforms used to drop modified grenades and mortar rounds from altitude onto infantry and light vehicles operate from commercial off-the-shelf hardware and draw their ammunition demand from the same grenade and mortar round chemistry as conventional infantry use, creating a second demand stream on those nodes that conventional consumption modeling does not account for.

Long-range strike drones, the Shahed and Lyuty equivalents that both sides have used against infrastructure and rear-area targets, carry warheads of 40 to 50 kilograms in Comp B or similar compositions, contributing approximately 144 tonnes each of RDX and TNT demand at scenario blended tempo.

Counter-drone operations, which at Ukrainian-conflict density involve significant expenditure of autocannon ammunition against drone targets, are estimated to add a consumption uplift of roughly 15 to 20% on autocannon ammunition categories, based on Ukraine war consumption data. That translates to roughly an additional 200 tonnes of RDX and 500 tonnes of additional nitrocellulose demand from those categories.

Aggregated across all drone categories, the additions to the scenario chemistry totals are in the range of 1,100 tonnes of additional RDX per year, 600 tonnes of additional TNT, and roughly 500 tonnes of additional nitrocellulose from counter-drone autocannon uplift. These additions move the revised scenario figures to approximately 35,900 tonnes per year of RDX, 17,050 tonnes of TNT, 25,870 tonnes of nitrocellulose, and 11,512 tonnes of ammonium perchlorate.

The structural conclusions of the gap analysis are unchanged by the drone additions. The gaps were catastrophic before accounting for drones and remain catastrophic after. The drone additions are relevant because they confirm that modeling ammunition chemistry demand without drones systematically understates demand at every node, and that the scale of the understatement is not trivial.

The drone platform supply chain dependency, the Chinese components problem, is a planning consideration of equivalent urgency to the explosive chemistry gaps, but it sits outside the conventional ammunition chemistry frame and therefore requires explicit treatment.

Ukraine built its drone manufacturing base in approximately two years from near-zero to 200,000 units per month under wartime conditions. The constraint was components, and specifically the Chinese-origin components that Ukraine was able to access through commercial and gray-market channels that would not be available to a European nation in open conflict with Russia and in a deteriorated relationship with China.

A sovereign European FPV manufacturing program, producing at the scale a sustained conflict would require, would need to source or produce brushless motors, battery cells, camera modules, and flight controllers from non-Chinese supply chains, and no such supply chains exist at the required volume today.

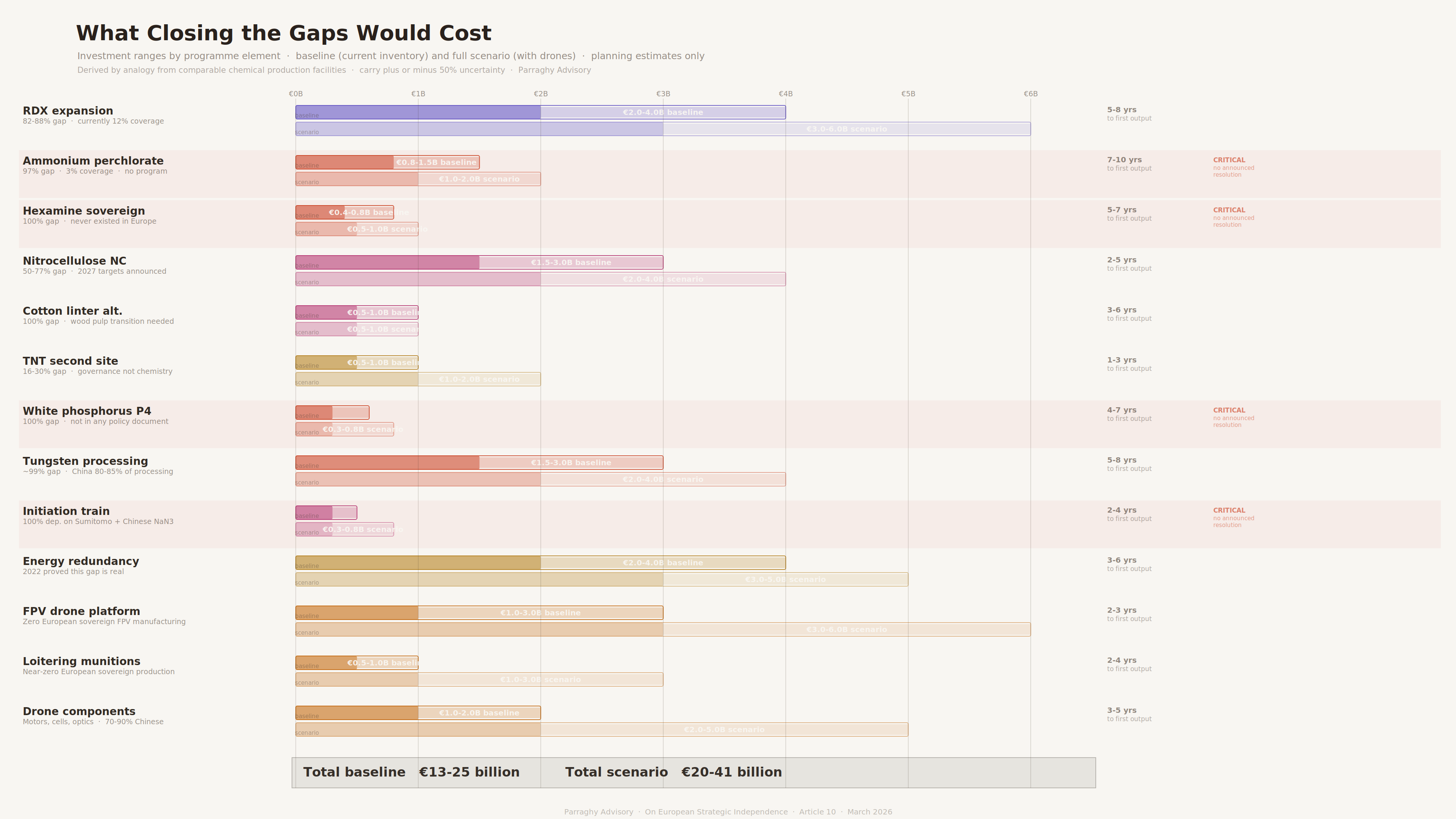

What closing the gaps would require

Assessed against current documented European inventory, without scenario expansion, the minimum chemistry investment required to establish sovereign European production capacity at conflict-adequate levels falls in the range of 13 to 25 billion euros.

These figures are planning estimates derived by analogy from publicly available cost data for comparable chemical production facilities, and carry substantial uncertainty, likely of plus or minus 50% or more depending on site conditions, regulatory requirements, and whether existing industrial land can be repurposed or greenfield construction is required.

The range itself reflects that uncertainty in addition to differences in facility design costs, permitting timelines, and the cost premium of building at European regulatory standards.

These figures cover ammunition only and do not account for the investment required to establish the sovereign European supply chains for the pharmaceutical active ingredients and fertilizers.

What it costs

The diagram below shows the full decomposition of that investment across all programme elements, with baseline and scenario cost ranges alongside the estimated time from decision to first operational output for each.

The per-element breakdown is as follows. Expanding European RDX production from the targeted 3,000 to 5,000 tonnes per year to a level adequate for current inventory demand requires the construction of new production facilities at an estimated cost of 2 to 4 billion euros.

A second European TNT production site, which would address the governance failure described above rather than a physical infrastructure shortage, would cost approximately 500 million to 1 billion euros and would have a shorter construction timeline than any other element in the program. Nitrocellulose expansion to the levels announced for 2027 would cost approximately 1.5 to 3 billion euros, and if executed, would cover current inventory demand at the lower end of the uncertainty range.

A military-scale ammonium perchlorate facility, which does not currently exist in Europe, would cost approximately 800 million to 1.5 billion euros and would require 7 to 10 years from design to validation. Sovereign hexamine production at European scale, which has never existed, would cost approximately 400 to 800 million euros. White phosphorus production from domestic phosphate rock processing would cost approximately 300 to 600 million euros.

Tungsten ore processing to cover the penetrator demand from European tank and GMLRS inventories would require approximately 1.5 to 3 billion euros in mining and refining infrastructure.

The initiation train investments, covering lead styphnate and lead azide production at conflict-adequate scale with domestically sourced or allied precursors, would cost approximately 300 to 500 million euros. Energy system redundancy for the ammonia and nitric acid chains, meaning the infrastructure required to maintain output during energy price disruptions of the type that occurred in 2022, would cost approximately 2 to 4 billion euros. Those items sum to the baseline 13 to 25 billion euro range.

At full conflict scenario scale, the investment figure rises to 20 to 41 billion euros, with the additional 7 to 16 billion covering the increment in chemistry capacity required to serve a fully mobilized force structure, plus the drone manufacturing investments. The drone platform and component program alone, covering FPV manufacturing sovereignty, loitering munition production, and the supply chain for motors, cells, and optics, would require 6 to 14 billion euros across all elements, because none of the required supply chains exist at European scale today. Two aspects of this investment picture deserve attention beyond the headline figures.

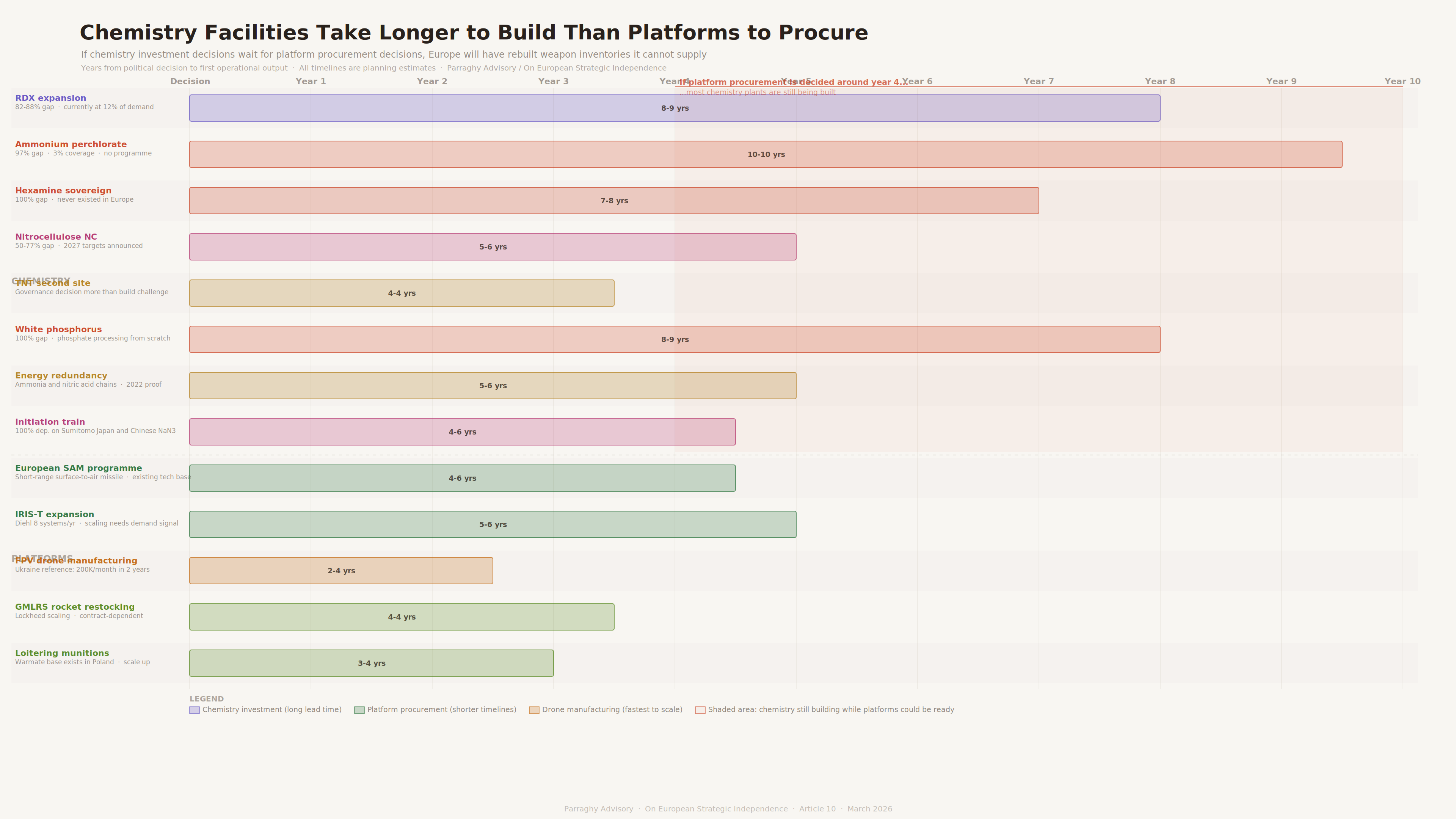

Why the sequence matters more than the total

Chemistry facility lead times are longer than platform procurement lead times for most systems in the inventory. An ammonium perchlorate plant requires 7 to 10 years from design to operational validation. An RDX facility requires 5 to 8 years. A hexamine program, starting from no existing European production base, requires 5 to 7 years minimum.

By comparison, a European short-range surface-to-air missile program, building on existing missile engineering knowledge, could realistically reach production within three to five years, which is still shorter than the timelines for most chemistry facility programmes. IRIS-T battery procurement is measured in years, not decades. FPV drone manufacturing at scale, based on the Ukrainian reference, can be achieved in 2 to 3 years under deliberate industrial policy.

This sequencing means that if chemistry investment decisions are deferred until platform procurement decisions have been made, Europe will find itself in the position of having rebuilt weapon inventories that it cannot supply with the chemistry they require. The chemistry investment decision must precede or run strictly in parallel with platform decisions, because the chemistry lead times are longer and the investments are therefore more time-sensitive.

Which gaps are most urgent

The second observation concerns which gaps are most urgently under-addressed relative to their strategic significance. The ammonium perchlorate gap is 97% and has no announced resolution. The hexamine gap is 100% and has no announced resolution. The white phosphorus gap is 100% and is not discussed in any European ammunition sovereignty document reviewed for this research.

The initiation train dependency on Sumitomo and on Chinese sodium azide is absolute and is essentially unknown outside specialist defense procurement circles. These are not the largest investment line items in the program. But they are the ones where a disruption would be most immediately and completely debilitating, because they are categorical dependencies with no substitutes and no buffers.

How this infrastructure needs to be governed

The third observation concerns how this infrastructure should be designed and governed once the investment decision is made, because the governance model chosen at the outset will determine whether the infrastructure actually provides the resilience it is intended to provide.

The instinct in democratic systems is to treat large public investment programs with full parliamentary transparency, because that is the appropriate governance model for civilian infrastructure. However, it is not the appropriate governance model for critical infrastructure, such as the explosive chemistry production infrastructure, and applying it uncritically will produce facilities that are visible, locatable, and therefore targetable before they have operated for a single day.

An adversary conducting pre-conflict reconnaissance does not need to penetrate classified systems to identify a single large hexamine plant or a single ammonium perchlorate facility if that facility was permitted through public regulatory processes, announced through a parliamentary budget debate, and reported on by the defense industrial press. A single-site facility with a published address and known production capacity concentrates strategic vulnerability in a way that appropriately distributed and classified infrastructure would not, because a potential adversary does not need to penetrate classified systems to identify it as a priority target in the event of open conflict.

The production infrastructure that closes these gaps needs to be designed from the beginning around two principles that standard industrial policy does not apply. The first is geographic and operational distribution across multiple sites in multiple countries, with each site holding partial but not complete production capacity for any given compound, so that the destruction or disruption of any single facility does not eliminate European sovereign production capacity entirely. The second is that the operational detail of that network, meaning the specific locations, the facility hardening specifications, the redundancy architecture, the production capacity at each site, and the supply chain routing between sites, should be designed, held, and managed by personnel with appropriate security clearances drawn from military and intelligence communities rather than published in the procurement documentation that parliamentary budget approval normally requires.

This is a distinction that democratic systems already make, and make routinely, for critical infrastructure, to which military infrastructure belongs.

A parliament that approves a defense budget authorizes expenditure within agreed program envelopes without receiving, or being entitled to receive, the precise coordinates of submarine berths, the hardening specifications of command bunkers, or the communications architecture of nuclear command and control facilities. The same principle applies here. Parliament approves the total investment in sovereign explosive chemistry production infrastructure, within a program envelope defined at an appropriate level of abstraction. The operational design of that infrastructure is then held by the relevant military and intelligence authorities under existing security frameworks, subject to oversight mechanisms that operate at the classification level appropriate to the material.

What this requires in practice is not something that individual European nations can provide by applying their existing national classification frameworks to facilities within their own borders. A single nation cannot commission, fund, or govern a distributed multi-site network spanning multiple countries as a unified classified program, because it has no authority over the facilities, supply routes, and operational coordination that exist outside its own jurisdiction.

The redundancy design that makes this infrastructure genuinely resilient, with no single country holding complete production capacity for any critical compound, inter-site supply routing that survives the loss of any one node, network architecture that an adversary cannot map from the destruction pattern of the first strike, is a European-level design problem that requires a European-level commissioning authority.

That authority does not exist.

The European Defense Agency can coordinate member state cooperation but cannot commission classified military-industrial infrastructure across borders. The EU's existing ammunition production instruments, the Act in Support of Ammunition Production and the European Defense Industry Reinforcement through common Procurement Act, operate through standard public procurement frameworks that, while they contain some national security exemptions, are not designed to protect the operational detail of classified military-industrial networks spanning multiple countries.

NATO holds operational classification authority over military installations but does not have the investment commissioning authority over civilian industrial infrastructure that this program would require. No existing European institution sits at the intersection of investment authority, cross-border jurisdiction, and classification power that commissioning this network would demand.

This is the same structural gap identified in the previous article for pharmaceutical production infrastructure. The pharmaceutical active ingredient manufacturing network that Europe needs to sustain battlefield medicine at conflict scale also requires a European commissioning authority that does not currently exist, for the same reasons. In both cases, the problem is not that individual nations lack the will or the legal frameworks to classify military infrastructure within their own borders. It is that the infrastructure the problem requires is inherently European in scale and therefore inherently beyond what any individual nation can commission, and the European institutional architecture has not been designed to fill that role.

Building the institutional authority is therefore the prior condition for building the infrastructure, and in this author's assessment it is the more difficult of the two problems, because physical infrastructure follows from engineering and capital, while institutional authority requires the kind of deliberate political design that European states have historically been reluctant to undertake in the domain of defense. The legal and treaty frameworks required to create a European body with the mandate to commission classified cross-border military-industrial investment, with budget authorization flowing from member state parliaments to that body at appropriate levels of abstraction, and with operational governance held by cleared personnel drawn from member state military and intelligence communities, do not currently exist and would require deliberate political design to create.

Why that institutional authority does not exist, yet

The reason this design does not exist is that European nation states have not wanted to give up the control that such an authority would require. Transferring the commissioning and governance of industrial military infrastructure to a body that is not directly accountable to their own voters means accepting that someone else holds decisions that touch their national survival.

That resistance is both deeply rooted and strategically rational, and runs considerably deeper than a preference for national procurement processes. It is rooted in national identities, which in Europe formed over centuries, and in some cases millenia, of shared history, war, ethnic homogenization, cultural consolidation, and the collective search for meaning that eventually produced populations willing to defend themselves as distinct peoples.

Nations that emerged from that process do not easily hand the decisions closest to their survival to a body whose legitimacy they did not themselves build. The institutional gap described above is a symptom of that deeper condition rather than a cause in its own right. I will address that condition in future articles looking at identity, demography, birthrates, immigration, social cohesion, institutional legitimacy, and what European solidarity can and cannot realistically be built on given the political and demographic realities that exist across the continent today.

The structural argument

The European ammunition sovereignty debate is conducted in platform terms because platforms are what the defense industrial complex prices, what governments procure, and what ministers can point to. Chemistry is harder to explain, harder to photograph, and harder to attach to a ceremony or a delivery schedule, but it is the layer where the actual constraints operate, and it is the layer that has been systematically under-examined because the institutional attention and the analytical frameworks have been calibrated to the wrong level of the supply chain.

Several of the gaps documented here are not recent. Cotton and hexamine have never been sovereign. White phosphorus has never been part of the conversation. Lead styphnate has one significant global supplier and that supplier is Japanese, which has been true for many decades.

While the post-Cold War defense spending reduction made everything worse, these are structural features of an industrial system that was designed around peacetime supply chain economics rather than around the resilience properties required for sustained conflict.

The 2022 energy event, which the final diagram traces from natural gas through the cascade to explosive chemistry outputs, provides a documented, real-world demonstration of a structural vulnerability that is otherwise difficult to make vivid. The scenario that maximizes European military demand for ammunition chemistry is also the scenario most likely to compress the upstream supply of that chemistry, because the same geopolitical conditions that produce a high-intensity European conflict are also the conditions most associated with energy supply disruption. Planning for those scenarios as though they are independent is a modeling error with operational consequences.

Ukraine has provided, at enormous cost, the most comprehensive real-world dataset that exists for what modern high-intensity conflict actually consumes at industrial scale. The layer this analysis finds most systematically under-examined is chemistry, required at scale, continuously, under conditions that simultaneously compress the supply of its own root inputs, with drones drawing on the same chemistry as conventional weapons and introducing their own platform supply chain dependency on components that are almost entirely produced in China.

Addressing any one of those dimensions while leaving the others unaddressed produces the appearance of progress rather than the substance of it, because each unsolved dimension remains a point at which the entire system can be stopped.