This is part B of the twelfth article in a series where I examine the structural conditions that would need to change for Europe to function as a genuinely independent strategic actor.

In the previous article I established that the three supply chains traced across Parts IX through XI draw from one chemical-industrial system, that governing it requires a single cross-domain mandate at European level rather than three separate domain programs, and that the dependencies this system contains that cannot be substituted under conflict conditions belong in the category that warrants reduction rather than management.

In this article I work through what the reduction of those dependencies requires to build, sizing each facility type the system needs against European conflict-scenario demand, establishing the order in which construction has to happen, and examining how a program of this scale gets financed.

The investment and sequencing the mandate requires

The most direct way to size what this mandate must build would be to take each of the findings from the previous three articles and treat them as three separate sizing exercises. Pharmaceutical sovereignty requires its own dedicated chemistry, ammunition production requires its own, fertilizer sovereignty requires its own, and the total investment is simply the sum of the three. This approach has the advantage of matching how the three articles were written and how European institutions are currently organized, with separate authorities each responsible for sizing their own domain.

The visual of the bulk chemical system that opened this article is illustrating that that approach is wrong. Ammonia and nitric acid sit at the center of all three supply chains, which means that sizing them separately means sizing the same upstream production capacity three times.

Instead, I had to answer how much of the underlying bulk chemical system needs to exist, built to what scale, and distributed in what way, to cover all three downstream chains under conflict conditions with enough margin that losing part of the system does not collapse it.

The margin itself is worth fixing before anything else. The demand figures I use throughout this section describe what Europe needs across all three downstream chains combined. This is what makes the combined sizing exercise different from the sum of three separate ones, since the convergence nodes, ammonia above all, serve all three chains from the same production capacity. A system built to exactly the combined figure has no slack. If any facility is lost to a strike, a cyberattack, or an energy disruption, the system falls below what it needs the moment that happens. Adding 20+ percent above conflict-scenario demand is what allows the system to absorb a loss and keep functioning, and that margin is assumed throughout everything that follows.

I was explicit in Parts IX and X that the demand figures carry plus or minus 50 percent uncertainty, because they are derived from a potential conflict-scenario with projections involving casualty volumes, infection profiles, resistance escalation rates, and firing rates, all of which are inherently uncertain. I use the mean of those projections throughout Parts XII-A to XII-C, because the mean is the most defensible single figure to work from when the range is symmetric and the tails are equally plausible.

However, a facility count derived from mean demand could be too low or too high if actual conflict conditions land at the edge of that range rather than at its center. What the sizing exercise in this section produces is therefore a central-estimate investment case for pharmaceutical and ammunition chemistry, not a fixed prescription. The fertilizer figures sit on firmer ground and the facility counts derived from them are not subject to the same caveat. The mandate I argued for in Part XII-A is what must hold the authority to adjust the pharmaceutical and ammunition components upward if the conflict scenario clarifies toward the upper end of that range, rather than treating the central estimate as a ceiling.

Intuitively, most would assume that cost scales with capacity in a straight line, so that a plant half the size costs half as much and produces half the output. If that were true, distributing production across twice as many sites would be free. However, it is not true. Halving the size of a chemical plant typically reduces its cost to roughly two-thirds rather than one-half, because the infrastructure that makes a plant function, the pressure vessels, the control systems, the energy connections, the safety engineering, does not shrink at the same rate as the production volume.

Engineers refer to this relationship as the six-tenths rule, which means that as the production capacity or the size of a given equipment or facility increases, the capital cost related to it increases non-linearly due to the economies of scale. It is the reason why we have been building increasingly bigger nuclear power plants, and why the bulk chemical industry settled with large facilities over the past several decades. That also means that every decision in this section about how many facilities to build, and how large each one should be, is a decision about how much of a premium we are willing to accept and pay for the ability to survive losing one of the systems its parts.

At this point one might wonder whether that premium is the same for every type of facility the bulk chemical system requires, and treat them as variations of one calculation. They are not, which is why I treat each of the five facility types that follow separately.

The shared upstream infrastructure, what all three chains require first

If each of the three supply chains were governed and sized separately, in practice, we would be optimizing the performance of the parts of the system instead of the performance of the system as a whole, which would result in a misaligned system. And since we would assume a smaller production volume, there's the risk that the facilities commissioned would be smaller versions of the same facility type, each paying the six-tenths penalty for being smaller than it needed to be.

The alternative is to size the ammonia requirement once, across all three chains together, and to build facilities large enough that the six-tenths penalty is minimized. A world-scale facility of this kind does not stop at ammonia. The same natural gas feedstock and the same process engineering that produce ammonia also produce, as integrated co-products, the other compounds the three chains require from this part of the system.

Urea is produced by combining the carbon dioxide that ammonia synthesis generates as a byproduct with some of the ammonia itself, and feeds the fertilizer chain directly. Ammonium nitrate and its derivatives, including the calcium ammonium nitrate and urea-ammonium-nitrate solutions that fertilizer applications require, are produced from the same ammonia stream. And methanol, produced from the same synthesis gas that the ammonia step begins from, feeds forward through formaldehyde into hexamine, the precursor that the explosive compounds RDX and HMX require for the ammunition chain.

One facility type, built at world scale, therefore covers the nitrogen chemistry needs of all three downstream chains from a single feedstock and a single site design. Yara's complex at Sluiskil in the Netherlands, producing up to 1.9 million tonnes of ammonia per year across three production trains, is what a facility of this kind looks like in operation. European ammonia demand for fertilizers alone runs at approximately 12.5 million tonnes per year. Covering that demand at Sluiskil's scale requires between six and seven complexes before any margin is added. Adding a 25 percent conflict margin brings the number to eight.

The cost of each complex depends on how much of the integrated product range it includes. The ammonia synthesis trains themselves run to roughly 1 billion euros for a Sluiskil-scale set of three trains. A fully integrated site, including the urea, ammonium nitrate, methanol, and hexamine process units that make the site useful to all three chains rather than only the fertilizer chain, runs to roughly 4 to 4.5 billion euros. Eight such sites represent an investment in the range of 32 to 36 billion euros.

Sulfuric acid, the second upstream shared dependency

The natural next question, having established that one facility type covers the nitrogen chemistry for all three chains, is whether the same logic extends to the other major upstream compound the visual identifies as a convergence point. Sulfuric acid feeds the phosphoric acid that fertilizer production requires and the nitration processes that several explosive compounds require, which makes it a shared dependency in the same sense that ammonia is.

The difference is the feedstock. Ammonia synthesis begins from natural gas. Sulfuric acid begins from elemental sulfur, and in practice almost all of that sulfur is recovered as a byproduct of refining crude oil and natural gas, specifically from the desulfurization step that removes sulfur from those streams before they can be used further.

A sulfuric acid plant therefore belongs adjacent to refining capacity, where its feedstock already exists as a byproduct stream. This means sulfuric acid requires its own facility type sited according to its own logic, not an addition to the nitrogen complex.

Sulfuric acid production is also one of the oldest continuous chemical processes still in operation at industrial scale, and the cost curve reflects that maturity. The six-tenths penalty for building smaller units is less severe here than for nitrogen chemistry, which gives more flexibility in how many plants to build without the cost consequences becoming as steep. World-scale units run at around 1.0 to 1.2 million tonnes per year. European demand is approximately 7.6 million tonnes per year. At the upper end of that reference scale and with the 25 percent margin added, eight plants are required. At 150 to 250 million euros per plant, the total comes to 1.2 to 2.0 billion euros.

Phosphoric acid processing, a capacity without sovereignty

The next compound we can identify on the bulk chemical system visual as a major convergence point is phosphoric acid, which feeds the granulated fertilizer products European agriculture depends on, specifically diammonium phosphate, monoammonium phosphate, triple superphosphate, and single superphosphate. The natural assumption, following the pattern of the previous two sections, would be that building enough phosphoric acid processing capacity closes this gap the same way the nitrogen and sulfur capacity closes theirs.

Sizing that capacity is straightforward. A phosphoric acid complex combines sulfuric acid with phosphate rock to produce phosphoric acid, which is then processed further into the fertilizer products listed above. European demand for phosphoric acid runs at approximately 2.75 million tonnes per year. At a reference train size of 0.55 million tonnes per year, and with the 25 percent margin added, six complexes are required, at 400 to 600 million euros each, for a total of 2.4 to 3.6 billion euros.

However, this section differs from the previous two. The complexes that process phosphate rock into usable fertilizer do nothing about where phosphate rock itself comes from. Morocco and the Western Sahara hold approximately 72 percent of the world's known phosphate reserves, while Europe holds almost none.

What this means is that phosphoric acid is the first compound in this section where the answer is not simply a facility count. The six complexes are part of the answer, and 2.4 to 3.6 billion euros belongs in the total, but the rock dependency itself requires a different approach. What that approach could be like and require is something this article returns to later.

Munitions nitration, where redundancy is nearly free

The three facility types covered so far are all bulk chemical infrastructure, producing millions of tonnes per year, where the six-tenths rule makes distributing production across more sites a real cost. The munitions-specific nitration plants that produce nitrocellulose, the explosive compound trinitrotoluene, commonly abbreviated TNT, and the explosive compounds RDX, sometimes called hexogen, and HMX, which is also called octogen, are a different category entirely. Given that these plants are already small relative to bulk chemistry, I had to settle how many of each to build.

The bare-demand approach would be to size each plant type to just cover European demand plus the margin, using as few plants as the reference scale allows. For nitrocellulose, European demand is approximately 25,400 tonnes per year and reference defense-scale plants run at 10,000 to 15,000 tonnes per year, so two to three plants would cover demand plus margin. The same logic applied to TNT, at approximately 16,400 tonnes per year against the same 10,000 to 15,000 tonne reference scale, also points to one or two plants.

The problem with stopping there is the same problem I identified in the articles Part IX to Part XI for concentrated production generally. Two or three plants of a given type means that losing even one of them removes a large fraction of total capacity at once, and these are the compounds that sit at the foundation of every barrel-fired weapon Europe uses. So, how could we ensure that losing some of them still leaves the system functioning?

Here is where the fact that these plants are already small relative to bulk chemistry becomes the deciding factor. Because nitrocellulose, TNT, and RDX and HMX plants already sit close to the scale where the six-tenths penalty flattens out, going from two or three plants to five does not multiply the cost the way going from eight nitrogen complexes to sixteen would. Five plants, each built to roughly 25 percent of European demand, means that losing any two of the five still leaves three plants running, which works out to 75 percent of demand still being met. That is the built in resilience that ensures that under pressure the system, and with it our collective defense, does not collapse. The cost is a modest rather than a considerable premium.

Applying this to nitrocellulose, five plants at roughly 100 to 200 million euros each represent a total investment of 500 to 700 million euros. For trinitrotoluene, five plants sized the same way, against demand of approximately 16,400 tonnes per year, represent 600 to 900 million euros. For RDX and HMX, the highest-hazard and most complex of the three because the nitration step that converts hexamine into RDX operates at the extreme end of what continuous chemical processes can safely manage, reference plants run smaller, at 10,000 to 12,000 tonnes per year, against demand of approximately 34,800 tonnes per year. Five plants sized the same way represent 1.2 to 1.8 billion euros.

Across all three sub-types, the total is approximately 2.3 to 3.4 billion euros, and what that buys is fifteen defense-industrial facilities across three distinct types, each governed under military classification, distributed so that no single strike removes more than one facility of any type, and each sized so that losing two facilities of a given type still leaves the system above 75 percent of conflict-scenario demand for that compound.

White phosphorus, the fixed-cost exception

White phosphorous is the compound European military smoke munitions require and that Europe currently produces in zero quantity. The demand for it runs at approximately 2,000 to 5,000 tonnes of elemental phosphorus per year, which is a small figure compared to all other demand figures. One might be wondering which logic would be applicable for this plant type, and what makes this distinct from the other types.

At this scale this compound is produced in an electric arc furnace, a technology similar in character to aluminum smelting, where the dominant cost is not the chemical process itself but the energy infrastructure, specifically the grid connection and the power supply commitment that the furnace requires. For an electric arc furnace, the grid connection is close to a fixed cost regardless of how large or small the furnace itself is. A second plant would roughly double the grid-infrastructure commitment.

One could build one large facility sized to 125 percent of demand and accept the single-point-of-failure risk, compensating for it with a strategic stockpile of finished munitions. That approach is cheaper, but it creates a targeting asymmetry. A single facility producing all of Europe's white phosphorus supply is the obvious priority target for any adversary.

The alternative would be two facilities of equal size, each producing between 60 and 70 percent of demand, giving a combined output of 120 to 140 percent of total demand across both sites. Symmetric sizing removes the targeting asymmetry, because neither facility is more valuable to destroy than the other. If one is lost, the surviving facility still produces 60 to 70 percent of demand, which is a degraded but functioning position rather than a complete collapse.

And critically, adding one or more additional production line(s) within the surviving facility, which already has the grid connection, the site infrastructure, and the workforce in place, is a fundamentally different rebuild timeline than reconstructing a destroyed facility. The resilience this configuration provides therefore comes not only from the surviving facility's output but from the speed at which its capacity can be expanded once the immediate pressure is understood.

So, how does the six-tenths relationship apply here?

The formula is:

C2 = C1 × (S2 / S1)^0.6

Where:

- C1 = the capital cost of the baseline full-scale facility

- S1 = the capacity of the baseline full-scale facility, expressed as 100 percent of European demand

- S2 = the capacity of each of the two mid-sized facilities, expressed as 60 to 70 percent of European demand

- C2 = the estimated capital cost of each mid-sized facility

No publicly available capital cost data exists for white phosphorus facilities of this type, as the only comparable operating facilities are in China's Yunnan and Guizhou provinces, Kazakhstan's Chimkent plant, and the now-closed Albright and Wilson site in Whitehaven in the United Kingdom, none of which have published construction cost figures. The baseline of 300 to 500 million euros for a facility sized to European demand is therefore a by-analogy estimate, derived from the electric arc furnace cost structure the process requires rather than from a cited facility cost, and carries wider uncertainty than the figures for facility types where a named reference exists.

Because that baseline carries both a lower and upper figure, and because the symmetric multi-site design introduces a second variable in the form of the 60 to 70 percent sizing range, four scenarios are needed to cover the full range of what two slightly smaller facilities could realistically cost.

Substituting the figures:

- At 60% capacity, lower baseline: 300,000,000 × (0.60 / 1.00)^0.6 ≈ 221,000,000

- At 60% capacity, upper baseline: 500,000,000 × (0.60 / 1.00)^0.6 ≈ 368,000,000

- At 70% capacity, lower baseline: 300,000,000 × (0.70 / 1.00)^0.6 ≈ 242,000,000

- At 70% capacity, upper baseline: 500,000,000 × (0.70 / 1.00)^0.6 ≈ 403,000,000

As evident from the calculation above, two facilities each sized symmetrically to meet 60 to 70 percent of European demand will cost between 442 to 806 million euros in total across both sites, doubling the per-facility figures the calculation above produces, depending on where in that sizing range the design falls and which end of the baseline cost estimate is applied as the basis.

Active pharmaceutical ingredient campuses and its cost-curve

The compounds involved, primarily the penicillin-derived antibiotics that I identified in Part IX as irreplaceable under conflict conditions, running from Penicillin G through the two semi-synthetic intermediates the manufacturing chain requires, 6-aminopenicillanic acid and 7-aminocephalosporanic acid, to the finished carbapenems and monobactams, are produced in quantities measured in hundreds of tonnes per year rather than millions. The entire European conflict-scenario demand for this chain is, in volume terms, orders of magnitude smaller than the volumes of ammonia or sulfuric acid, which might suggest that a single campus, or at most two, would comfortably cover it with capacity to spare.

Is one campus enough?

While a single campus does cover the volume, it also constitutes a single-point-of-failure. If the one facility producing Europe's carbapenems and monobactams is destroyed, disrupted, or otherwise taken offline, the result is the complete absence of European production for drugs that, as I established in Part IX, sit at the bottom of the antibiotic treatment ladder with no clinical substitute below them. For every other compound, losing a facility means a degraded system. For this one, losing the only facility means no system at all, for however long it takes to bring production back online. That outcome rules out one campus on its own.

Instead of asking how many campuses produce the required volume, which a single site already does, I asked how much loss of production capacity is tolerable for compounds that cannot be substituted?

I laid out in Part IX the sequence of antibiotics a wounded soldier moves through as infections prove resistant to whatever was tried before. For each of those antibiotics I have set a coverage threshold, which is the minimum share of worst-case demand that supply has to meet before the gap between supply and demand starts producing deaths that a strategic stockpile and a triage protocol would have otherwise prevented.

The threshold for the carbapenems were set at an 80 percent threshold, ceftazidime-avibactam at 90 percent, and the Step 4 last-resort drugs, cefiderocol and aztreonam-avibactam, at 100 percent with no fallback below it, because for the patients who reach these through that sequence, no other drug works. Further, I explained why I set those thresholds where I did rather than lower, why the production architecture behind them has to be distributed across enough sites that losing any one of them still keeps total output above the threshold I set, which is precisely the constraint this subsection's campus count has to satisfy.

The simplest way to satisfy all four thresholds at once would be to build campuses that each produce the full range of compounds across the chain, so that no single threshold depends on a facility the others do not also have access to. While this has an obvious appeal, it also has an obvious flaw once take the perspective of an adversary. A facility that produces everything is a facility worth destroying entirely, because a single successful strike degrades all four coverage thresholds simultaneously rather than just one.

That kind of design does not match how this kind of manufacturing works. The fermentation process that produces Penicillin G and the chemical semisynthesis steps that convert it through 6-APA and 7-ACA into finished carbapenems and monobactams use different organisms, equipment, and validated procedures. These are closer to two distinct manufacturing capabilities than one continuous line.

What resolves both problems at once is organizing the network as regional clusters rather than single campuses, with each cluster containing a fermentation and semisynthesis facility sited close enough to each other to keep transportation and logistics cost low, but built as physically separate sites within that region.

Proximity does more here than reduce transport cost. The fermented intermediate that the semisynthesis facility needs has its own handling and stability requirements, and close enough siting means a replacement delivery can arrive within hours of an order being placed, not the next day. That matters when a batch fails, material is contaminated, or a deviation in a process forces a facility to stop and wait. A semisynthesis site that can receive fresh material within a few hours of placing an order keeps idle time to a minimum and validated production capacity in use, rather than sitting unused for a day or more while a distant supplier processes and delivers a replacement.

That responsiveness reduces how much buffer stock either facility needs to hold against their production processes, and most importantly, enables faster recovery from the unplanned failures that continuous biological production is prone to in the first place. Held inventory of a biological intermediate is capital sitting idle and a quality risk in something this time-sensitive. The proximity this cluster design provides reduces what each facility needs to build and finance to operate, not only what it costs to ship between them.

What remains is how many clusters this network needs, and the answer depends on the regulatory and validation overhead that makes each facility within a cluster expensive in the first place. It is a cost per facility regardless of its size and therefore does not shrink as the network grows.

The buffer of underutilized capacity

There is a second resilience mechanism available and it changes how much the stockpile this section eventually arrives at needs to hold. Every facility within a cluster is built with more production capacity than it normally uses. A facility designed to produce a volume which, for example, constitutes 30 percent of total demand at its absolute maximum is not run at that maximum under normal conditions.

Continuous fermentation and the semi-synthesis steps that follow it are typically operated somewhat below their designed ceiling, to allow for batch changeovers, quality checks, and equipment upkeep without excessive wear from constant maximum output. Industry benchmarking data for fermentation-based bioprocessing, measured through what the industry calls Overall Equipment Effectiveness, abbreviated as OEE, commonly places sustained output in the range of 65 to 80 percent of nameplate capacity, even among well-run sites. A facility designed and built to produce a maximum output that constitutes about 30 percent of European demand would, on that basis, normally be utilized to produce an output that covers between 19.5 and 24 percent of that European demand.

That means if one facility or cluster is disrupted or destroyed, the surviving clusters do not need to expand or rebuild their facilities to absorb the lost output. Each can simply run closer to the capacity it was already built for. This needs only a change in how intensively already-approved facilities are operated. Obviously, that is a faster path back to higher output than building a new production line or reconstructing a destroyed facility.

What is the role of a strategic reserve?

This means the stockpile's primary job is to bridge the shorter gap between a disruption occurring and the surviving clusters reaching the higher end of what they were already built to produce. The longer, multi-year rebuild timeline only becomes the relevant constraint in the less likely case that the surviving clusters cannot absorb the loss on their own, for instance if multiple clusters are lost within a short period of time rather than one. Sizing the stockpile this way still follows the worst-case planning standard I stablished in Part IX, since it plans for the harder scenario where it matters, while not inflating the reserve to a depth the more common single-loss scenario does not require.

One question worth raising is whether the timeline to (re-)build a facility could compress the way Ukraine's drone production did, scaling from workshop output to industrial volume in roughly a year. Their old procurement model, which was built for peacetime accountability and slow sequential review, was replaced under pressure with a new model designed for the problem they faced.

The seven to ten year figure I established in Part IX is the timeline under the current civilian procurement process, where each review step waits for the formal close of the one before it. A facility commissioned under a redesigned process of that kind, with compressed, parallelized, and more risk-tolerant decision-making in place of the sequential model, could plausibly move faster than that floor, in principle by a wide margin.

The reason this section still sizes the stockpile against the slower figure rather than an optimistic compressed one is that how much compression actually happens depends on whether that redesigned process gets built at all, and on the political will and institutional capacity to build it, none of which has been tested at this scale.

Worst-case planning means building against the path that can be verified today, not the path a future redesigned process might deliver. The classification framework I propose in Part IX, having these facilities designed, commissioned, built, and governed under either the military or intelligence communities, would make it possible to design a new process. This of course does not guarantee the compression happens, or by how much, which is why the seven to ten year floor remains the basis for what this section sizes the stockpile against, while the surge capacity built into five clusters is designed specifically to reduce how often the system has to rely on that slower path.

Beyond the costs

Five clusters represent a total investment of approximately 1.5 to 2.2 billion euros across the ten facilities involved. The stockpile, sized against the shorter surge window rather than the full rebuild timeline, adds a further line item the combined total at the end of this section accounts for separately.

The design I propose is not only an answer to an adversary who might target it. Each cluster, by combining fermentation and semisynthesis facilities within close reach of each other, becomes a regional concentration of two complementary forms of expertise rather than one, with the clean room engineering, the regulatory knowledge, and the specialized workforce each facility requires sitting close enough together to reinforce each other.

Five such clusters distributed across the continent seed exactly the kind of complementary, self-reinforcing industrial activity that earlier in this article I identified as what makes a location durable, and they do it as a direct consequence of the same design choice that resolves the targeting vulnerability, not as an unrelated side effect of it.

Potassium, what doesn't require a facility

I established in Part XI that potassium is a sourcing problem rather than a production capacity problem, that the reserves exist in accessible territory held by allied or neutral states, and what has been missing is the institutional decision to hold enough in reserve to bridge a disruption.

The solution to this issue is a strategic reserve. The instinct would be to size it against the difference between allied-supply and total European demand, on the reasoning that Canada and other genuinely allied producers will continue supplying their share and that the reserve only needs to cover what that allied supply cannot provide. While that reasoning is internally consistent, it contains an assumption I have not allowed myself anywhere else in this series, that supply from allied sources continues uninterrupted under the conditions that make the reserve matter most. Atlantic shipping routes are not guaranteed under the conflict scenario of Part IV to VII, and a reserve sized against the difference between allied-supply and total European demand relies on exactly the supply it is supposed to protect against failing.

There is a second reason to reject the comfortable sizing. A disruption of our potassium supply before it is applied in the spring planting window leads to a shortage in food supply that cannot be corrected later in the season. We cannot grow food retrospectively. The lag between a supply disruption and its visible consequence to the civilian population is one growing season, and the consequence is reduced food availability for the continent's entire population.

That irreversibility is the same logic I applied in Part IX to battlefield medicine, where the planning standard was determined by the asymmetry between the recoverable error and the irrecoverable one. It applies here with longer lag times and broader population impact. This is the one supply chain in this article where I cannot allow myself the assumption that allied supply will be available, because the cost of that assumption being wrong is not recoverable within the timeframe that matters.

The second instinct would be to express the reserve depth in calendar terms, a six-month reserve or a three-month reserve, the way most strategic reserves are described. That framing is useful for commodities whose demand is roughly continuous across the year. Potassium is not such commodity.

Fertilizer application is concentrated in two windows, spring pre-planting and autumn post-harvest soil conditioning, with very little demand in the periods between them. A reserve holding six months of average annual demand might, under certain circumstances, not be sufficient to cover one of the two high-demand application phases it was supposed to bridge. What matters is whether the reserve can cover one full annual application cycle from the moment supply is disrupted, regardless of when in the calendar that disruption arrives, which requires sizing against full annual demand rather than a fraction of it.

At total European demand of approximately 15.74 million tonnes of potash ore per year and current market prices of approximately 350 to 450 euros per tonne, the one-year reserve procurement cost is approximately 5.5 to 7.1 billion euros. It is the only item in this section that is a one-time acquisition rather than a facility, but it is not a small figure.

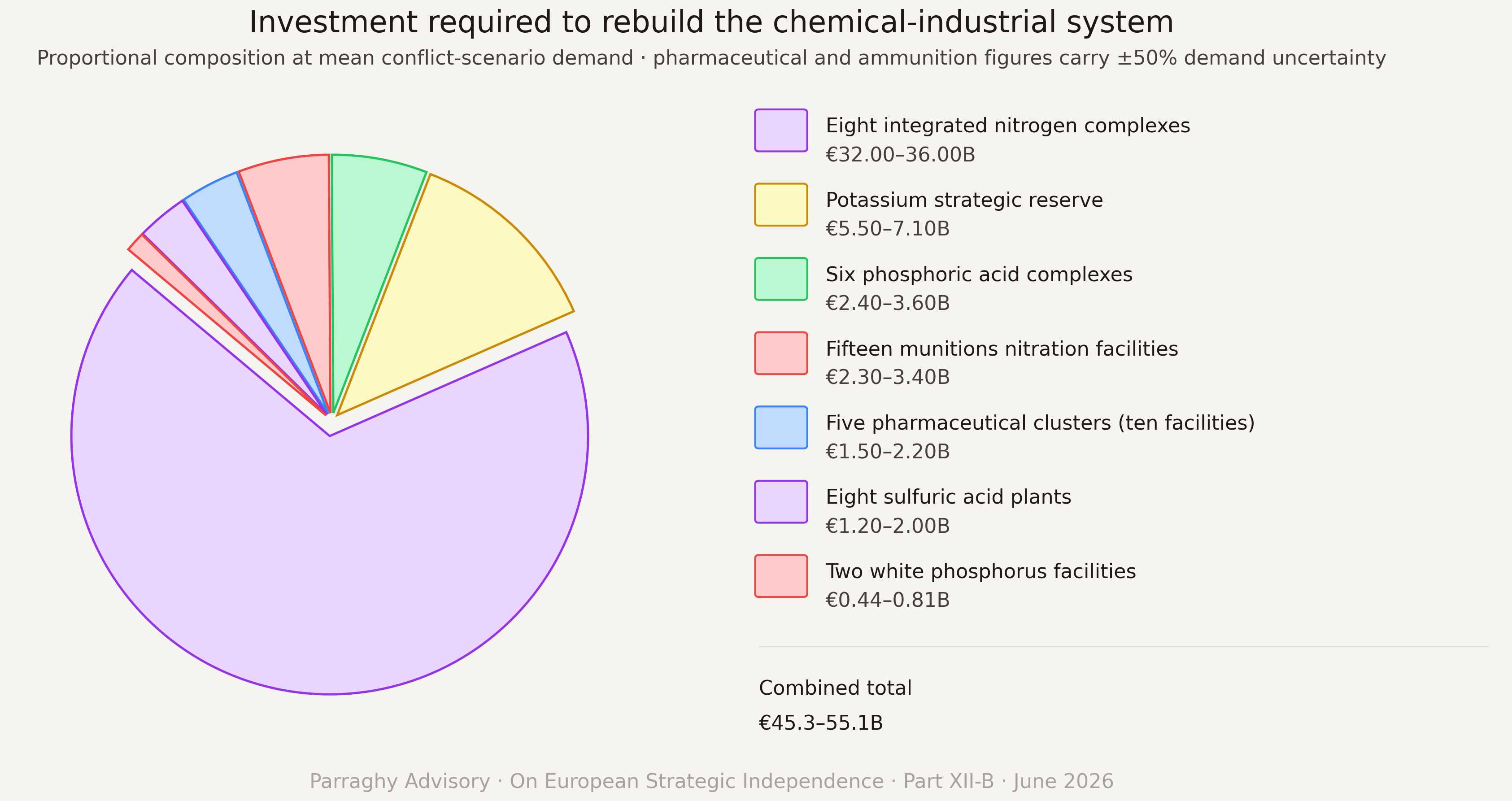

The combined figure

Each of the previous sections arrived at a number by asking what that part of the system requires, and the constraint that decided each number differed by facility type. Putting those numbers together produces a combined picture.

- Eight integrated nitrogen complexes come to 32 to 36 billion euros.

- Eight sulfuric acid plants come to 1.2 to 2.0 billion euros.

- Six phosphoric acid complexes come to 2.4 to 3.6 billion euros.

- Fifteen munitions nitration facilities across the three sub-types come to 2.3 to 3.4 billion euros.

- Two white phosphorus facilities, sized symmetrically to remove the single-site targeting risk, come to approximately 0.44 to 0.81 billion euros.

- Five pharmaceutical clusters, each containing a fermentation facility and a semisynthesis facility, ten facilities in total, come to approximately 1.5 to 2.2 billion euros.

- The potassium strategic reserve comes to 5.5 to 7.1 billion euros.

The total is approximately 45.5 to 55.1 billion euros.

European institutions do fund parts of what the seven items above describe, but only the finished, downstream parts each sector's mandate covers. The EU Critical Medicines Act funds pharmaceutical manufacturing capacity, and ASAP and EDIRPA fund European ammunition production capacity. What none of these, or any other European instrument, fund, or has ever been positioned to fund, is the upstream bulk chemistry this section has spent its length sizing. No European institution's mandate covers that shared industrial base layer underneath it.

Three separate programs, each sizing and commissioning their own share of this chemistry, would cost considerably more than 45.5 to 55.1 billion euros, since each would build its own ammonia capacity at whatever scale its own demand justified, smaller than the eight world-scale sites this section arrives at and therefore subject to the same six-tenths penalty applied throughout.

That said, the more important difference is not the price, but what three separate programs mistake the system for. There has only ever been one system, the bulk chemical base this article opened by establishing, and three programs each optimizing their own downstream share of it are not building three systems, they are optimizing three fragments of the same one in isolation from each other, which is the dysfunction this article has been describing throughout. A single mandate would, for the first time, treat the system as what it is, classified under the framework I argued for earlier in this article to govern the whole network under one set of rules, optimizing the performance of the system as a whole.

The combined figure above covers the seven facility types and the one strategic reserve I have sized in this section. It does not include the upstream feedstock investments that several of those facilities require and that the mandate must also commission. The fifteen munitions nitration facilities depend on hexamine and cotton linters that have no European sovereign production, and I documented both in Part X as 100 percent gaps. The eight nitrogen complexes and the broader ammonia chemistry infrastructure depend on natural gas, and the transition to green ammonia that eliminates that dependency on natural gas is a separately scoped program whose cost I do not claim to size here. And the ammunition chain requires ammonium perchlorate at military scale, with a 97 percent difference between sovereign production and demand which I documented in Part X, which belongs in this investment section but has not been included here because I have not sized it yet with the same facility-by-facility rigor I applied to the seven items above.

The combined figure is the minimum infrastructure investment the system requires at mean conflict-scenario demand for the pharmaceutical and ammunition components, not the total, and that the mandate I argued for in XII-A is what determines what else gets added to it.

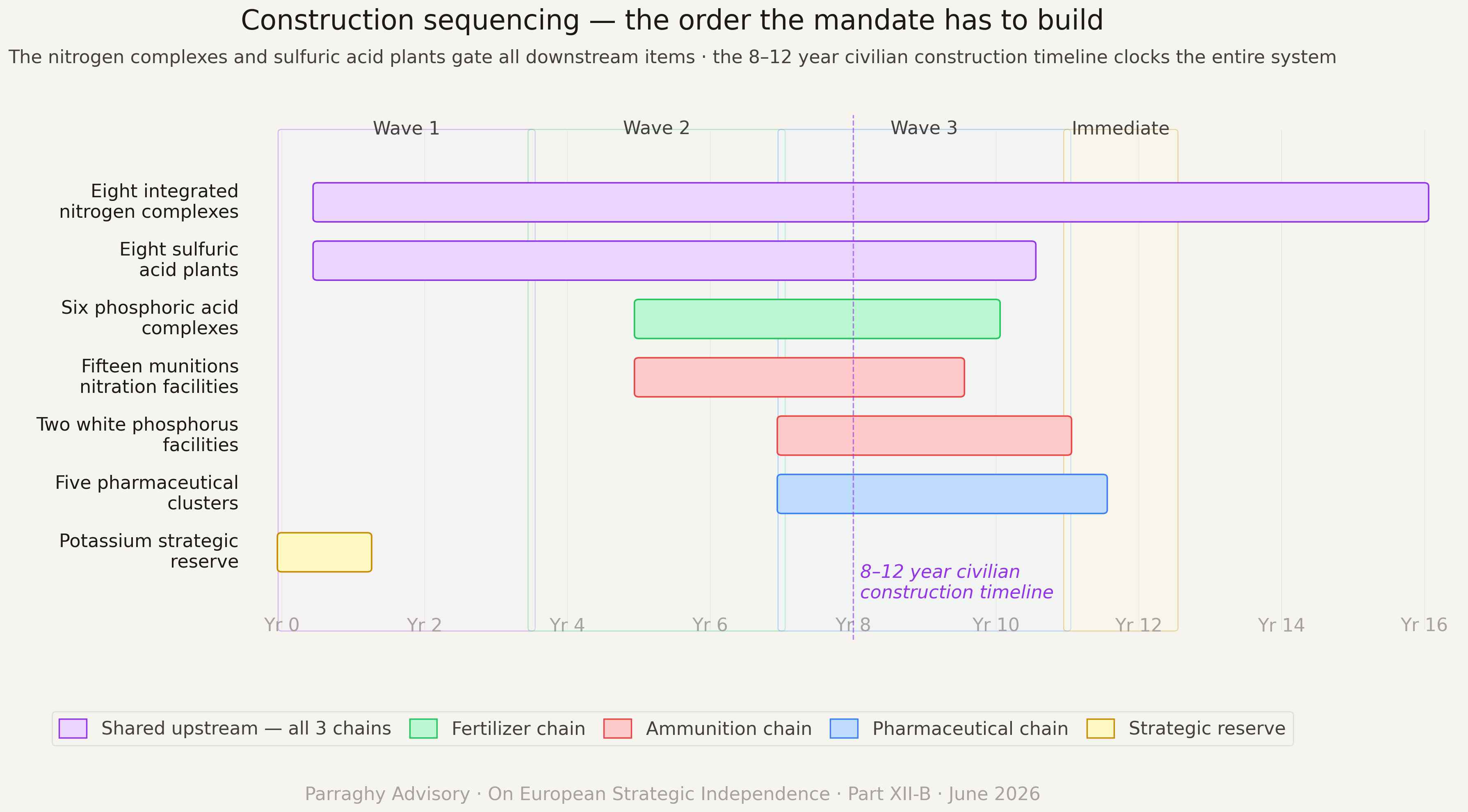

The construction, but in what order?

The investment figure in this article assumes all seven components get built, but not in what order. I established in Part X that the ammonia synthesis trains and the integrated nitrogen complex carry a lead time of eight to twelve years from a decision being made to the facility producing at scale. That is the timeline under the current civilian permitting, environmental review, and procurement procedures.

A nitrogen complex commissioned under that framework, with permitting and review compressed or run in parallel rather than sequentially, could plausibly move faster than the eight to twelve year floor, in principle by a meaningful margin. How much faster depends on political will, institutional capacity, and how a redesigned process would actually function, none of which has been tested at this scale, which is why I use the slower figure as the planning basis for the sequencing question that follows, in keeping with the same worst case standard I have applied throughout this series.

The instinct would be to start all seven components at once, on the reasoning that the total cost is what it is regardless of order, so waiting on any one item only delays the system as a whole. That instinct does not survive contact with what each of them depends on. Starting all seven at once means six of the seven sit waiting for the nitrogen complex regardless of when their own construction began, because nothing downstream of ammonia can run at meaningful scale until ammonia exists at meaningful scale.

This points to a sequential build order rather than a simultaneous one. The nitrogen complexes and the sulfuric acid plants come first, because they carry the longest lead times and depend on nothing else in this list. The phosphoric acid complexes and the munitions nitration plants come next, since they depend on the upstream chemistry being available but carry shorter individual construction timelines once that chemistry exists. White phosphorus and the pharmaceutical clusters can run in parallel with this second wave, since neither depends on the nitrogen or sulfur chemistry the way the others do. The potassium reserve is the one item that could begin immediately, since it requires no construction at all, only a procurement decision and the legal mandate I described earlier in this article.

This means that the eight to twelve year lead time on the nitrogen complex is the clock the entire system runs on. Every year that decision is delayed is a year added to when the full forty to forty eight billion euro system becomes operational, not just to when the nitrogen complex itself does, and I have established in Parts VI to VII of this series what the window for that delay looks like.

Funding: who is paying for this, and how?

My findings in this article split into two separate financing questions. The first question is who pays to build productive capacity that does not yet exist. The second question is who holds a reserve of finished output once that capacity exists and is producing. These are different problems with different answers, and the Swiss legal mandate based model I described for potassium only answers the second one.

On construction

The instinct, and the one closest to how Europe currently organizes large capital projects, is for each member state to fund its own share, whatever facilities sit within its own borders or serve its own domestic demand. I established why this fails on capital grounds earlier in this article.

That said, there is a second failure specific to this I must point out. A nationally funded nitrogen complex gets sized against that nation's own demand, which reintroduces the penalty from the six tenths relationship I outlined earlier, since a facility sized to one nation's share of demand sits well below the world scale that makes the eight site figure economically defensible in the first place. National funding faces a capital problem and by recreating it, a fragmentation problem, which I was arguing against.

The alternative is financing organized at the European level, against the European total, but a legal mandate to hold something cannot substitute for the capital this requires. That said, direct public financing alone reproduces a version of the same capital constraint problem, just moved from the national level to the European one, since forty to forty eight billion euros entirely from public budgets still competes against every other public spending priority across the continent. The more useful question is how to make this attractive enough that private and institutional investors want to participate, so the public share of the bill is something Europe can sustain.

A few instruments, not mutually exclusive, do this.

- Joint European debt and lending through the European Investment Bank, of the kind already used for other continent-scale capital programs, using the facilities themselves as collateral.

- Direct co-investment from the industries that will eventually use the output, probably the most realistic path for at least part of the total, since those industries already have capital at stake in their own downstream production.

- A public-private structure where government capital absorbs the first loss and private capital is recruited for the safer, senior position, supported by tax incentives that improve the return on holding equity in this kind of infrastructure, accelerated depreciation for capital intensive chemical facilities, loan guarantees that let private lenders extend debt at lower risk because a public mandate backstops default, and direct subsidy specifically for the conflict margin portion of each facility's capacity, since that share of output exists for a public good reason rather than a commercial one.

Whichever combination a European mandate settles on, it operates under the same classification rules I established for the physical infrastructure earlier in this article, which rules out the standard transparent procurement structures Europe currently uses for civilian infrastructure spending.

On strategic reserves

Switzerland requires, through a cooperative structure that any firm operating in the industry must join, that the industry collectively hold a defined quantity of finished product, with the cooperative deciding internally how that obligation gets distributed among its members. Nothing about that mechanism is specific to food or to potassium. Once the nitrogen complexes are producing, the firms operating in that space can be required to hold a reserve of finished ammonia and nitric acid through exactly this structure.

The same applies to all finished products, whether those are acids, compounds, and pharmaceutical active ingredients, which I covered in a previous section of this article, where the surge capacity and stockpile logic I worked through there is, in effect, is this same mechanism applied to one item in advance of naming it as a general one.

Potassium is the one item where the reserve question is the entire answer, because no new production capacity has to be built before the reserve can exist. For the other six items, the mandated reserve sits on top of the financed construction. The industry holds finished output in reserve once the facilities exist, the same way Swiss importers hold grain once it has been milled, while the facilities themselves are paid for through the construction financing I just described in this section.

What the next part will cover

I examine in Part XII-C what reducing the dependencies means for the actors currently holding the leverage those dependencies represent, work through the scenarios that worst-case planning requires accounting for, and address what the one dependency I identified in this article as unreshorable requires as a response.

Citation: Parraghy, D. (2026). On European Strategic Independence, Part XII-B: What reshoring the chemical-industrial system would require, https://parraghyadvisory.com/articles/what-reshoring-the-chemical-industrial-system-would-require.html